Both Toby and Donna are 62 years old. Toby works in sales and Donna works as a secretary. After Toby lost his job in 2010, they applied for a loan modification with Bank of America to lower their mortgage payments. They asked City Pulse to withhold their real names because Toby is interviewing for a new job soon and fears his potential employer might look down on him.

“When we applied for the loan modification, we were very proactive,” Toby said. “We called them all the time to ask them if they had received the paperwork. Within a month or so they said everything was going through. They assured us that nothing would happen to us, that we were protected. They said if we didn’t make loan payments in the meantime, no problem, they would take care of it.”

The couple started making payments on the modification in December 2010 after it was finalized, but in May 2011 — even after making every single payment — they got a letter in the mail from Bank of America saying the foreclosure process was starting on their home. Shortly after that, a notice was posted on their door telling them to vacate the house. They were notified that Fannie Mae had bought their house at a sheriff’s sale.

At the advice of a neighbor, the couple contacted Ingham County Register of Deeds Curtis Hertel Jr., who went to bat for the couple. He went to court and was quickly able to prove that the two had made their payments and that the sale of the house to Fannie Mae was illegal. Somewhere along the line in Bank of America’s communication network, the bank had dropped the ball, Hertel said. Within two weeks, the eviction was canceled and the sale of Toby’s and Donna’s house was rescinded in June 2011.

“The day after the hearing, (Toby) called me and said that was the first good night of sleep that he’d gotten in more than a month,” Hertel said. “He thought he was going to lose his house for something he didn’t do. The mental health, the physical health, the things it does to people — pain and suffering is what we’d call it in court — it’s sick.”

While they were able to keep their house, Toby and Donna’s lives were thrown into chaos throughout the process. They’re still recovering to this day.

“We were packing our house up and thinking the threat of being evicted was there and was real. So, we spent four to five weeks packing up our house, not sleeping, worried as hell about what was going to happen,” Toby said. “We carried all of our medications in the car, along with suitcases full of clothes, and took our valuables out of the house in case we came back to a locked house with all of our furniture in our yard. It was pretty damn stressful.”

Donna said she had nightmares about them having to live in a cardboard box on the street. She gained 40 pounds due to the stress.

“At this point in your life, you’re looking to retire, not start all over. We are now at the point where we can’t retire, we don’t have the money. So, it really did feel like it affected everything we had planned for all our lives,” Donna said. “So, here we are, we’re both 62, and we’re not even sure how much longer we’re going to have to work until we can retire. It’s not what people typically think their life is going to be, especially when they’ve saved all their life. But we are fortunate to have this house and we owe that all to Curtis.”

By the numbers

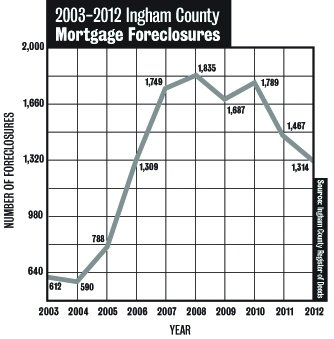

Since 2003, there have been over 13,000 mortgage foreclosures in Ingham County, according to figures from the Register of Deeds Office. While the numbers are improving, that doesn’t change the story for people who are burdened with the stress and anxiety that comes with facing the possibility of losing the homes they’ve built their lives around.

“With mortgage foreclosures, the good news is that they’re dropping in Michigan,” said Neeta Delaney, director of the Michigan Foreclosure Task Force, a statewide coalition providing information on the foreclosure crisis and advocating for foreclosure policy changes. “The bad news is if you look at 2012 to 2013, we lost 70,000 homes to foreclosure, which makes us the third highest state for mortgage foreclosures in the country.”

In Hertel’s opinion, the biggest reason that foreclosures shot up over the past decade was the repeal of the federal Glass-Steagall Act of 1999, which allowed banks to do investments in addition to dealing with loans and savings.

“When we removed that barrier, we made banks these giant things that could actually sell housing as stock,” Hertel said.

Before the foreclosure crisis — during “the good years,” as Hertel called them — the average number of people losing their homes to mortgage foreclosure in the county was 400 and 500 annually, he said. In 2008, at the peak of the foreclosure crisis, 1,835 Ingham County homes went into foreclosure.

With bigger institutions came more opportunities for breakdowns in communication and attempts to make shortcuts through practices like robo-signing. Mortgage fraud can take numerous forms, ranging from banks refusing to give qualified applicants a modification to forged mortgage documents. And then there are mortgage help scammers, which exist outside the realm of banks. According to the Federal Bureau of Investigation’s 2010 Mortgage Fraud Report, Michigan ranked in the top 11 states for “suspected mortgage fraud activity.”

Amid these statistics, it’s easy to forget that behind the numbers are stories of everyday people whose lives have been thrown into chaos because of suspect mortgage foreclosure practices.

Abby

In January 2010, Abby, a 53-year-old small business owner from Meridian Township, fell behind in her mortgage payments because her “deadbeat” ex-husband was grossly behind in child support. Two months later, she was able to negotiate a lower payment modification with her bank. She made three payments over the next three months. Her lender accepted the first payment and cashed the check in May of that year, but the lender decided to hold the second and third payment without telling her until August.

“This was when I tried without luck to get any answers — eventually, I got a letter in October informing me that my modification was denied because I was now too far behind in payments,” Abby wrote in an email. “I was now 10 months behind because they refused to take my payments.”

“They set me up,” said Abby, who asked City Pulse not to reveal her identity because of her children.

Abby got help through Hertel’s office and was able to stay in her house after the case went to Ingham County Circuit Court. Judge Rosemarie Aquilina ruled in her favor in 2011.

“The biggest thing for (Abby) was that she had an agreement with the bank, but they wouldn’t accept payments,” Hertel said. “They basically made it a very difficult process. Eventually (the lender’s) lawyer filed a document in court admitting there was a modification.”

Foreclosure Fraud Hotline

Toby and Donna’s story, along with the discovery of forged mortgage documents in his office, inspired Hertel to create the Foreclosure Fraud Hotline in June 2011. Through the program, folks like Abby received legal assistance to help keep her house.

The program is a partnership between Hertel’s office, the Ingham County Board of Commissioners, the Ingham County Treasurer’s Office and Legal Aid of South Central Michigan. In June 2011, Ingham County commissioners approved $60,000 to fund the program, which aims to give legal aid to people who may be facing fraudulent mortgage foreclosure.

Hertel said the hotline has helped over 250 people stay in their homes by battling banks and lenders in the courts over the past two years. He said his office will go before the commission in the next month or two to ask for additional funding.

Legal Aid of South Central Michigan provides legal services to low-income residents in Barry, Clinton, Eaton, Ingham, Livingston and Shiawassee counties, but the organization also works with the Foreclosure Fraud Hotline to help represent people of all income levels who are facing mortgage foreclosure.

Since the service began, attorneys with the program have seen “all sorts of horrific things,” said Kellie Maki, managing attorney for the Lansing office of Legal Aid of South Central Michigan. “I almost don’t know where to begin.”

A month-and-a-half ago, Maki dealt with a situation involving an elderly woman in Lansing who, while she was negotiating a modification with the Bank of New York Mellon, came home one day to find that her house had been completely emptied of her belongings by a securing company hired by the bank. She said all of her belongings have since gone missing and the company hired to clear the house can’t locate her property. Maki is helping prepare a lawsuit against the bank and has filed a police report about the situation.

Unfortunately, foreclosure fraud is “really common,” Maki said.

“I think if someone is being foreclosed on, the idea that the lender has done everything properly and has followed the legal process almost never happens,” she said. “Rarely do I see a case that comes through my door where something hasn’t gone wrong in the foreclosure process. There’s always something that’s improper that’s happened.”

There have been several high-profile cases over the past year, which Hertel said show the rampant nature of foreclosure fraud.

In February, Loraine Brown, the former president of Georgia-based DocX, a mortgage document transferring company, pleaded guilty to racketeering charges stemming from “robo-signing,” a practice where employees were instructed to fraudulently sign an authorized person’s name on mortgage documents to move documents faster through the transfer process. Of the more than 1,000 fraudulently signed documents that were identified throughout the state, roughly 300 of them were filed in Ingham County, said Hertel, whose office first prompted the investigation.

The fraud doesn’t stop in Michigan. In 2012, Michigan and 48 other states (Oklahoma not included) were part of a $25 billion settlement with five major banks — Bank of America, Wells Fargo, JPMorgan Chase, Ally Financial and Citigroup — for fraudulent mortgage practices. It was reportedly the largest multi-state agreement since 1998, which involved nationwide tobacco settlements. Michigan received $97 million for the settlement and spent most of the money on programs to support blight elimination, free housing counseling services and assistance grants to homebuyers.

Hertel doesn’t believe the problem is going away soon. As part of his platform for state Senate to replace term-limited Sen. Gretchen Whitmer, D-East Lansing. Next year, Hertel said he wants to expand the hotline to a statewide program, which he said would cost $3.5 million and could help thousands of Michigan residents keep their homes.

“It’s one of the reasons I’m running,” he said. “We have proven that the banks are not 100 percent trustable. We need strong voices pushing for change for people who are losing their homes. To lose an asset with no due process is something that’s terrible. Michigan is one of the easiest states to foreclose in, and we’re making it easier, not harder.”

Shortening redemption

Michigan is a “foreclose by advertisement” state, which means banks and lenders don’t need to go before a judge to evict someone. They just have to post a notice on the door.

Because of this, Delaney, of the Michigan Foreclosure Task Force, said the state lengthened the redemption period on foreclosures to six months so people have time to prove the foreclosure is fraudulent in court, work something out with the bank, or sell the house in a short sale to save their credit.

But now the state Legislature is pushing for new timetables that foreclosure fraud fighters like Hertel, Maki and Delaney say will only put thousands more Michiganders on the street.

Legislation approved by the Senate Banking and Financial Institutions Committee on May 23 would shorten the foreclosure redemption period from six months to 60 days. The legislation comes as federal regulations starting next year will extend the negotiation period between banks and property owners before foreclosure from 90 to 120 days. It awaits a full Senate vote.

Sen. Darwin Booher, R-Evart, introduced the four-bill package. Booher was formerly sales manager at Citizens Bank and vice president of Bank One for a combined 40 years. He also chairs the Senate Banking and Financial Institutions Committee. The bills have the support of Michigan banking interests, which claim that the longer redemption period leads to abandoned properties, which contribute to blight, and that new federal regulations would help people avoid foreclosure. But for those who oppose the legislation, they say shortening the redemption period is unwise.

“The way I see it as county treasurer, the financial services industry in the last six years, as we’ve gone through this economic debacle, hasn’t improved much,” said Ingham County Treasurer Eric Schertzing, whose office partners with Hertel on the Foreclosure Fraud Hotline. “They mismanage paperwork, they don’t communicate and they can´t manage the volume of troubled mortgage holders they’re working with. I find it inhumane to think that the timeline on struggling homeowners who are trying to save their homes should be shortened.”

Phil and Paul

The mortgage foreclosure horror stories don’t stop with the banks and lending agencies losing paperwork, forging documents or just being difficult to deal with. For some facing mortgage foreclosure, they wind up becoming victims of mortgage help scammers who come promising to save their homes, but wind up stealing thousands of dollars from them.

Take the case of 53-year-old Phil Bachinski and 46-year-old Paul Levandowski of Lansing, who lost their home on Allen Street to foreclosure in December 2008 after they lost their jobs and the bank refused to negotiate a modification.

“When someone is facing foreclosure, it’s public record to everyone,” Bachinski said. “So, we had some attorneys and loan modification companies contact us. We were getting letters in the mail, telling us to contact them and send them money and they’d try to save our house. Well, we fell for one of them.”

The couple paid $1,000 — the last of their savings — to Foreclosure Resolutions LLC on the promise that the company would work with Wells Fargo to help them keep their house. Instead, the man who owned the company ran off with the money and they haven’t heard from him since.

The scam crippled the couple’s personal and financial lives. Because they had nowhere else to go, the two had to move into the basement of Levandowski’s father’s house, where they’ve been living since 2009. As for their finances, Levandowski recently filed for bankruptcy and Bachinski is in the process of filing.

The two had dreams of one day being foster parents or adopting a child, but those dreams have been crushed by their foreclosure crisis. Both of them have since found jobs and are saving up to get a new place of their own.

Delaney said there are two giveaways to spot a foreclosure help scam artist: One, there will be promises to save your home. Delaney said it’s impossible for anyone to guarantee that your home can be saved during a foreclosure. And two, they’ll want money up front.

So why is this happening? Are the big banks conspiring to push folks like Toby and Donna and single moms like Abby out of their homes for a profit? In Hertel’s opinion, the banks are too big for their own good.

“There are all sorts of nefarious ideas about why banks do what they do. I buy into some of them, but I think in general, their problem is more a matter of incompetence,” Hertel said. “I think the idea that they were too big to fail is wrong — I think they’re too big to run.”

Facing mortgage foreclosure? Contact the Michigan State Housing Development Authority Lansing office to seek out free housing counseling at (517) 373-8370. If you think you’ve got a case of foreclosure fraud, contact the Ingham County Foreclosure Fraud Hotline at (517) 676-7210.

Support City Pulse - Donate Today!

Comments

No comments on this item Please log in to comment by clicking here